Show the code

# Install necessary libraries for the experiment in the Colab environment

%pip install -q ccxt pandas thrml>=0.1.3 matplotlib seaborn![]()

NOTE: This notebook is configured to run on fresh historical data using a rolling window. The results will differ from the fixed dataset used in the article.

This work accesses publicly available trade data via exchange REST APIs through CCXT for independent non-commercial research. No raw exchange market data is stored persistently or redistributed; only aggregate experimental results are reported. Users should review each exchange’s terms of service before replication.

argmax on observed prices, and drops buckets where no venue has an observed price yet. This models a sell-side routing objective where the highest available price is optimal.| Parameter | Value | Description |

|---|---|---|

n_venues |

5 | Number of trading venues |

n_steps |

10,000 target | Rolling-window target before dropping buckets with no observed venue prices |

n_seeds |

200 | Independent runs for statistical significance |

discount_factor |

0.995 | Forgetting factor for non-stationary adaptation |

learning_rate |

0.05 | THRML learning rate |

steps_per_sample |

4 | Gibbs sampling thinning parameter |

propagation_damping |

0.3 | Mean-field signal propagation factor |

epsilon |

0.1 | ε-Greedy exploration rate |

# Install necessary libraries for the experiment in the Colab environment

%pip install -q ccxt pandas thrml>=0.1.3 matplotlib seaborn# --- STANDARD IMPORTS ---

import os

import sys

import time

from typing import NamedTuple, Tuple, Dict

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import jax

import jax.numpy as jnp

from jax import random, lax, vmap, jit

from thrml import SpinNode, Block, SamplingSchedule, sample_states

from thrml.models import IsingEBM, IsingSamplingProgram, hinton_init

import ccxt

print("--- HISTORICAL DATA EXPERIMENT ---")

print("This notebook fetches rolling historical window for replication on fresh data; results vary by execution time.")

print("Ready to go!")--- HISTORICAL DATA EXPERIMENT ---

This notebook fetches rolling historical window for replication on fresh data; results vary by execution time.

Ready to go!# Configuration settings for the experiments and agents

class ExperimentConfig(NamedTuple):

n_venues: int = 5 # Number of trading venues participating in the simulation

n_context_venues: int = 1

n_steps: int = 10000 # Target routing steps before dropping buckets with no observed venue prices

n_seeds: int = 200

window_size: int = 200 # Memory depth for incremental covariance tracking

beta: float = 1.0

n_warmup: int = 50

n_samples: int = 100

steps_per_sample: int = 4

discount_factor: float = 0.995 # Exponential decay factor for adapting to non-stationary shifts

learning_rate: float = 0.05 # Step size for bias and edge weight updates,

propagation_damping: float = 0.3

context_mode: str = "fixed"

damp_coupling: bool = Trueclass AgentState_CEG(NamedTuple):

successes: jnp.ndarray

counts: jnp.ndarray

class AgentState_CTS(NamedTuple):

alphas: jnp.ndarray

betas: jnp.ndarray

class AgentState_THRML(NamedTuple):

biases: jnp.ndarray

weights: jnp.ndarray

history_buffer: jnp.ndarray

history_ptr: jnp.ndarray

full_history_count: jnp.ndarray

cov_sum: jnp.ndarray

pair_counts: jnp.ndarraydef thrml_init(n_venues, window_size=200):

"""

Standardized initialization for THRML Agent State.

Ensures memory depth is consistent across experiments.

"""

return AgentState_THRML(

biases=jnp.zeros(n_venues),

weights=jnp.zeros((n_venues * (n_venues - 1)) // 2),

history_buffer=jnp.zeros((window_size, n_venues)),

history_ptr=jnp.array(0, dtype=jnp.int32),

full_history_count=jnp.array(0, dtype=jnp.int32),

cov_sum=jnp.zeros((n_venues, n_venues)),

pair_counts=jnp.zeros((n_venues, n_venues))

)

def thrml_update(state, outcomes, obs_mask, model_node_moms, model_edge_moms,

discount_factor, beta, learning_rate,

propagation_damping=0.3, damp_coupling=True):

"""

Perform the learning step using the THRML Ising model.

Uses a custom online update rule inspired by contrastive divergence.

"""

n_venues = state.biases.shape[0]

triu_idx = jnp.triu_indices(n_venues, 1)

# 1. Update Node Biases (h)

J = jnp.zeros((n_venues, n_venues)).at[triu_idx].set(state.weights)

J = J + J.T

influence = propagation_damping * learning_rate * beta * (J @ (outcomes * obs_mask)) * (1.0 - obs_mask)

new_biases = (state.biases * discount_factor) + (learning_rate * beta * (outcomes * obs_mask - model_node_moms * obs_mask)) + influence

# 2. Update Empirical Covariance (XX^T)

old_obs = state.history_buffer[state.history_ptr]

old_present = (old_obs != 0).astype(jnp.float32)

new_obs = outcomes * obs_mask

new_present = obs_mask

new_cov_sum = state.cov_sum - jnp.outer(old_obs, old_obs) + jnp.outer(new_obs, new_obs)

new_pair_counts = state.pair_counts - jnp.outer(old_present, old_present) + jnp.outer(new_present, new_present)

# 3. Handle Cyclic Buffer

new_buffer = state.history_buffer.at[state.history_ptr].set(new_obs)

new_ptr = (state.history_ptr + 1) % state.history_buffer.shape[0]

new_count = jnp.minimum(state.full_history_count + 1, state.history_buffer.shape[0])

# 4. Update Edge Weights (J)

emp_cov = new_cov_sum / jnp.maximum(new_pair_counts, 1.0)

emp = emp_cov[triu_idx]

pairs_observed = new_pair_counts[triu_idx] > 0

innovation = beta * learning_rate * (emp - model_edge_moms)

innovation = jnp.where(damp_coupling, innovation, 0.0)

new_weights = (state.weights * discount_factor) + jnp.where(pairs_observed, innovation, 0.0)

return AgentState_THRML(new_biases, new_weights, new_buffer, new_ptr, new_count, new_cov_sum, new_pair_counts)def select_among_max(key, scores, mask):

"""Choose venue by breaking ties randomly with small noise."""

noise = random.uniform(key, scores.shape, minval=-1e-6, maxval=1e-6)

return jnp.argmax(scores + mask + noise)

def build_thrml_infra(n_venues, config):

"""

Pre-calculates JAX-optimized graph structures.

Uses a fixed program structure that clamps the first n_context_venues.

Selection logic will permute nodes to satisfy this structure.

"""

nodes = [SpinNode() for _ in range(n_venues)]

edges = [(nodes[i], nodes[j]) for i in range(n_venues) for j in range(i+1, n_venues)]

schedule = SamplingSchedule(

n_warmup=config.n_warmup,

n_samples=config.n_samples,

steps_per_sample=config.steps_per_sample

)

# Static program structure for conditional selection: always clamp first K nodes

clamped_block = Block(nodes[:config.n_context_venues])

free_blocks = [Block([nodes[i]]) for i in range(config.n_context_venues, n_venues)]

dummy_model = IsingEBM(nodes, edges, jnp.zeros(n_venues), jnp.zeros(len(edges)), jnp.array(config.beta))

prog_conditional = IsingSamplingProgram(dummy_model, free_blocks, clamped_blocks=[clamped_block])

# Static program structure for joint update: no clamped nodes

serial_blocks = [Block([n]) for n in nodes]

prog_joint = IsingSamplingProgram(dummy_model, serial_blocks, clamped_blocks=[])

return {

'nodes': nodes,

'edges': edges,

'sched': schedule,

'prog': prog_conditional,

'joint_prog': prog_joint,

'full_block': [Block(nodes)]

}def get_context_index(context_venues, context_outcomes, n_venues, n_context_venues):

# Encode the full context tuple (venues + outcomes) into a single integer.

# Uses Horner's method for base-2N encoding: index = sum(state_i * (2N)^i)

# where state_i = venue_i * 2 + outcome_bit_i

outcome_bits = (context_outcomes > 0).astype(jnp.int32)

venue_states = context_venues * 2 + outcome_bits

def scan_fn(val, state_i):

return val * (2 * n_venues) + state_i, None

index, _ = lax.scan(scan_fn, 0, venue_states)

return indexdef ceg_init(config: ExperimentConfig) -> AgentState_CEG:

# Scale context space to (2N)^K to support multiple context venues

n_contexts = (2 * config.n_venues) ** config.n_context_venues

return AgentState_CEG(

successes=jnp.zeros((n_contexts, config.n_venues)),

counts=jnp.zeros((n_contexts, config.n_venues))

)

def cts_init(config: ExperimentConfig, prior_alpha: float=1.0, prior_beta: float=1.0) -> AgentState_CTS:

n_contexts = (2 * config.n_venues) ** config.n_context_venues

return AgentState_CTS(

alphas=jnp.ones((n_contexts, config.n_venues)) * prior_alpha,

betas=jnp.ones((n_contexts, config.n_venues)) * prior_beta

)

def ceg_select(state, key, cidx, routing_mask, epsilon=0.1):

"""Choose venue using tabular E-Greedy given context."""

n = state.counts.shape[1]

means = jnp.where(state.counts[cidx] > 0, state.successes[cidx] / state.counts[cidx], 0.5)

k_e, k_r = random.split(key)

act = jnp.where(random.uniform(k_e) < epsilon,

random.categorical(k_r, jnp.zeros(n) + routing_mask),

select_among_max(k_r, means, routing_mask))

return act

def ceg_update(state, cidx, venue, outcome, discount_factor):

"""Update expectations with global decay and local venue observation."""

s = state.successes * discount_factor; c = state.counts * discount_factor

return AgentState_CEG(s.at[cidx, venue].add(jnp.where(outcome > 0, 1.0, 0.0)), c.at[cidx, venue].add(1.0))

def cts_select(state, key, cidx, routing_mask):

"""Choose venue using Bayesian sampling given context."""

samples = random.beta(key, state.alphas[cidx], state.betas[cidx])

return jnp.argmax(samples + routing_mask)

def cts_update(state, cidx, venue, outcome, discount_factor):

"""Update posteriors with global decay and local venue observation."""

a = (state.alphas - 1.0) * discount_factor + 1.0; b = (state.betas - 1.0) * discount_factor + 1.0

return AgentState_CTS(a.at[cidx, venue].add(jnp.where(outcome > 0, 1.0, 0.0)), b.at[cidx, venue].add(jnp.where(outcome > 0, 0.0, 1.0)))# =============================================================================

# ROLLING WINDOW CONFIGURATION - FETCHES THE LATEST 10K-SECOND WINDOW

# =============================================================================

# This experiment uses a rolling 10,000-second window that automatically

# fetches the most recent available data. This ensures:

# 1. Data is fresh and reflects current market conditions

# 2. Results are based on up-to-date exchange behavior

# 3. Each run independently validates the experiment on new data

#

# The window ends 5 minutes ago (to ensure trade data has propagated)

# and spans exactly 10,000 seconds (~2.78 hours) backward from there.

# Buckets with no observed venue prices are dropped later before routing labels

# are created, so the final usable step count can be slightly smaller.

# =============================================================================

import time

from datetime import datetime, timezone

# Configuration

EXPECTED_STEPS = 10000 # Target 10k-second window before unusable-bucket trimming

BUFFER_SECONDS = 300 # 5-minute buffer to ensure data availability

# Calculate rolling window: ends 5 min ago, spans 10k seconds back

current_time_ms = int(time.time() * 1000)

HIST_END_MS = current_time_ms - (BUFFER_SECONDS * 1000) # 5 min ago

HIST_START_MS = HIST_END_MS - (EXPECTED_STEPS * 1000) # 10k seconds before that

# Display the window

start_dt = datetime.fromtimestamp(HIST_START_MS / 1000, tz=timezone.utc)

end_dt = datetime.fromtimestamp(HIST_END_MS / 1000, tz=timezone.utc)

print("=" * 65)

print("ROLLING WINDOW EXPERIMENT - LATEST 10,000-SECOND WINDOW")

print("=" * 65)

print(f"Window Start: {start_dt.strftime('%Y-%m-%d %H:%M:%S UTC')}")

print(f"Window End: {end_dt.strftime('%Y-%m-%d %H:%M:%S UTC')}")

print(f"Window Span: {EXPECTED_STEPS:,} seconds ({EXPECTED_STEPS:,} target buckets)")

print(f"Data Age: ~{BUFFER_SECONDS // 60} minutes old (buffer for propagation)")

print("=" * 65)

print("Note: Each run fetches fresh data, so results may vary slightly")

print("between runs due to different market conditions.")=================================================================

ROLLING WINDOW EXPERIMENT - LATEST 10,000-SECOND WINDOW

=================================================================

Window Start: 2026-03-18 12:42:30 UTC

Window End: 2026-03-18 15:29:10 UTC

Window Span: 10,000 seconds (10,000 target buckets)

Data Age: ~5 minutes old (buffer for propagation)

=================================================================

Note: Each run fetches fresh data, so results may vary slightly

between runs due to different market conditions.SYMBOL = 'BTC/USDT'

EXCHANGES = [

'binanceus',

'coinbaseexchange',

'kraken',

'bitfinex',

'bitstamp',

]

TIME_BUCKET_MS = 1000

TARGET_BUCKETS = 10000 # Rolling window: exactly 10,000 stepsdef sync_trades_hist(exchange_name: str, start_ms: int, end_ms: int) -> pd.DataFrame:

"""

Fetch historical trades from exchange for a specific time window.

"""

exchange = getattr(ccxt, exchange_name)({'enableRateLimit': True})

MAX_ITERATIONS = 1000

def get_trade_timestamp(trade):

if 'timestamp' in trade and trade['timestamp'] is not None:

return trade['timestamp']

if 'datetime' in trade and trade['datetime'] is not None:

from datetime import datetime

dt = datetime.fromisoformat(trade['datetime'].replace('Z', '+00:00'))

return int(dt.timestamp() * 1000)

if 'info' in trade:

info = trade['info']

if 'date' in info: return int(info['date']) * 1000

if 'timestamp' in info: return int(info['timestamp'])

raise KeyError(f"Could not extract timestamp")

try:

exchange.load_markets()

symbol = SYMBOL if SYMBOL in exchange.markets else "BTC/USD"

all_trades = []; seen_ids = set(); iterations = 0

last_batch_id = None

if exchange_name == 'kraken':

since = start_ms

while iterations < MAX_ITERATIONS:

iterations += 1

# Kraken's 'since' parameter expects milliseconds in CCXT

trades = exchange.fetch_trades(symbol, since=since, limit=1000)

if not trades or trades[0].get('id') == last_batch_id: break

last_batch_id = trades[0].get('id')

for t in trades:

ts = get_trade_timestamp(t)

tid = str(t.get('id', ts))

if start_ms <= ts <= end_ms and tid not in seen_ids:

seen_ids.add(tid)

all_trades.append({'timestamp': ts, 'price': float(t['price']), 'id': tid})

if not trades: break

last_ts = get_trade_timestamp(trades[-1])

if last_ts >= end_ms: break

try:

# Kraken returns 'last' id in nanoseconds, but ccxt expects ms for 'since'

raw = exchange.last_json_response

last_id_ns = int(raw['result'].get('last', str(last_ts) + '000000'))

since = last_id_ns // 1000000 # Convert ns to ms

except:

since = last_ts + 1000 # Fallback

time.sleep(exchange.rateLimit / 1000)

elif exchange_name == 'bitstamp':

since = start_ms

while iterations < MAX_ITERATIONS:

iterations += 1

# For Bitstamp, we request 'day' to get access to the 24h buffer

trades = exchange.fetch_trades(symbol, limit=1000, since=since, params={'time': 'day'})

if not trades: break

# Check for duplicates (if API ignores 'since' and returns latest trades repeatedly)

if trades[0].get('id') == last_batch_id:

break

last_batch_id = trades[0].get('id')

for t in trades:

ts = get_trade_timestamp(t)

tid = str(t.get('id', ts))

if start_ms <= ts <= end_ms and tid not in seen_ids:

seen_ids.add(tid)

all_trades.append({'timestamp': ts, 'price': float(t['price']), 'id': tid})

last_ts = get_trade_timestamp(trades[-1])

if last_ts >= end_ms: break

# Update since for next batch (if supported)

since = last_ts + 1

time.sleep(exchange.rateLimit / 1000)

elif exchange_name == 'coinbaseexchange':

cursor = None

while iterations < MAX_ITERATIONS:

iterations += 1

params = {'limit': 1000}

if cursor: params['after'] = cursor

trades = exchange.fetch_trades(symbol, limit=1000, params=params)

if not trades or (len(trades) > 0 and trades[0].get('id') == last_batch_id):

break

last_batch_id = trades[0].get('id')

for t in trades:

ts = get_trade_timestamp(t)

tid = str(t.get('id', ts))

if start_ms <= ts <= end_ms and tid not in seen_ids:

seen_ids.add(tid)

all_trades.append({'timestamp': ts, 'price': float(t['price']), 'id': tid})

oldest_ts = get_trade_timestamp(trades[-1])

# Try to get cursor from headers first (more reliable)

header_cursor = None

if hasattr(exchange, 'last_response_headers') and exchange.last_response_headers:

header_cursor = (exchange.last_response_headers.get('cb-after') or

exchange.last_response_headers.get('CB-AFTER'))

cursor = header_cursor or trades[-1].get('id')

if oldest_ts < start_ms: break

time.sleep(exchange.rateLimit / 1000)

else:

since = start_ms

while iterations < MAX_ITERATIONS:

iterations += 1

trades = exchange.fetch_trades(symbol, since=since, limit=1000)

if not trades or trades[0].get('id') == last_batch_id: break

last_batch_id = trades[0].get('id')

for t in trades:

ts = get_trade_timestamp(t)

tid = str(t.get('id', ts))

if start_ms <= ts <= end_ms and tid not in seen_ids:

seen_ids.add(tid)

all_trades.append({'timestamp': ts, 'price': float(t['price']), 'id': tid})

last_ts = get_trade_timestamp(trades[-1])

if last_ts >= end_ms: break

since = last_ts + 1

time.sleep(exchange.rateLimit / 1000)

print(f" + {exchange_name:<10}: Fetched {len(all_trades)} trades ({iterations} API calls).")

if not all_trades: return pd.DataFrame(columns=['timestamp', 'price', 'id'])

return pd.DataFrame(all_trades).drop_duplicates(subset=['id']).sort_values('timestamp')

except Exception as e:

print(f" [ERROR] {exchange_name}: {e}")

return pd.DataFrame(columns=['timestamp', 'price', 'id'])def process_market_data(dfs: Dict[str, pd.DataFrame], start_ms: int, end_ms: int):

"""

Process raw trade data into time buckets and calculate favorable outcomes.

Uses the specified historical time window.

IMPORTANT: Some exchanges only provide recent historical data (up to 24 hours).

- Partially missing data is handled with forward filling only to preserve causality.

- Leading buckets before an exchange's first observed trade use a strict sentinel value (0.0).

- Sentinel buckets are excluded from winner selection until at least one venue has an observed price.

- Completely missing exchanges remain unavailable for winner selection throughout the window.

"""

# Validate we have data from exchanges

available_exchanges = [ex for ex, df in dfs.items() if not df.empty]

missing_exchanges = [ex for ex, df in dfs.items() if df.empty]

if missing_exchanges:

import time

current_time_ms = int(time.time() * 1000)

hours_since_start = (current_time_ms - start_ms) / 3600000

print(f"[WARNING] No data from: {', '.join(missing_exchanges)}")

if hours_since_start > 24:

print(f" NOTE: Historical window starts {hours_since_start:.1f} hours ago.")

print(f" Some exchanges (e.g., Bitstamp) only provide up to 24h of historical data.")

if not available_exchanges:

print(f"[CRITICAL] No data from ANY exchange! Cannot proceed.")

return np.array([[]], dtype=np.float32), np.array([[]], dtype=np.float32)

if len(available_exchanges) < len(dfs):

print(f"[INFO] Proceeding with data from: {', '.join(available_exchanges)}")

print(" Missing exchange data stays unavailable until a real observed price exists.")

# Use the historical window boundaries

t_start = start_ms

t_end = end_ms

buckets = np.arange(t_start, t_end, TIME_BUCKET_MS)

print(f"[DATA] Processing {len(buckets)} time buckets ({t_start} to {t_end})")

for ex, df in dfs.items():

if not df.empty:

actual_start = df['timestamp'].min()

actual_end = df['timestamp'].max()

coverage_sec = (actual_end - actual_start) / 1000

target_sec = (end_ms - start_ms) / 1000

print(f" [COVERAGE] {ex:<10}: {coverage_sec:>7.1f}s of {target_sec:.0f}s ({coverage_sec/target_sec*100:>5.1f}%)")

else:

print(f" [COVERAGE] {ex:<10}: 0.0s (0.0%) - NO DATA")

master = pd.DataFrame({'bucket': np.arange(len(buckets)), 'ts': buckets})

# Missing or not-yet-observed venues keep a strict sentinel placeholder until

# they have a real observed price. Sentinels are excluded from winner selection.

fallback_price = 0.0

for i, (ex, df) in enumerate(dfs.items()):

if df.empty:

master[f'v{i}_p'] = fallback_price

print(f" {ex}: Using fallback price ${fallback_price:.2f} (no data available)")

else:

ex_d = df[(df['timestamp'] >= t_start) & (df['timestamp'] <= t_end)].copy()

if ex_d.empty:

master[f'v{i}_p'] = fallback_price

print(f" {ex}: No trades in window, using fallback price ${fallback_price:.2f}")

else:

ex_d['b_idx'] = ((ex_d['timestamp'] - t_start) // TIME_BUCKET_MS).astype(int)

ex_b = ex_d.groupby('b_idx').agg({'price': 'last'}).rename(columns={'price': f'v{i}_p'})

master = master.join(ex_b, on='bucket', how='left')

first_trade_bucket = int(ex_b.index.min())

master[f'v{i}_p'] = master[f'v{i}_p'].ffill().fillna(fallback_price)

print(f" {ex}: {len(ex_d)} trades mapped to buckets (causal fill from bucket {first_trade_bucket})")

prices = [f'v{i}_p' for i in range(len(EXCHANGES))]

values = master[prices].values

available_mask = values > fallback_price

valid_rows = available_mask.any(axis=1)

dropped_rows = int((~valid_rows).sum())

if dropped_rows:

print(f"[DATA] Dropping {dropped_rows} leading buckets with no observed venue prices.")

if not np.any(valid_rows):

print("[CRITICAL] No bucket contains an observed venue price after preprocessing.")

return np.array([[]], dtype=np.float32), np.array([[]], dtype=np.float32)

master = master.loc[valid_rows].reset_index(drop=True)

values = master[prices].values

available_mask = values > fallback_price

masked_values = np.where(available_mask, values, -np.inf)

max_vals = masked_values.max(axis=1, keepdims=True)

is_max = available_mask & (masked_values == max_vals)

np.random.seed(42) # Seed for reproducible tie-breaking among observed venues

best_venue = np.array([np.random.choice(np.flatnonzero(row)) for row in is_max])

for i in range(len(EXCHANGES)):

master[f'v{i}_r'] = np.where(best_venue == i, 1.0, -1.0)

master[f'v{i}_s'] = master[f'v{i}_r']

cols_r = [f'v{i}_r' for i in range(len(EXCHANGES))]

cols_s = [f'v{i}_s' for i in range(len(EXCHANGES))]

return master[cols_r + cols_s].values.astype(np.float32), master[prices].values.astype(np.float32)def thrml_select_conditional(state, key, cvs, cos, infra, config):

n = config.n_venues

triu_idx = jnp.triu_indices(n, 1)

# 1. Create permutation mapping CVs to the first K indices

priorities = jnp.zeros(n, dtype=jnp.int32)

priorities = priorities.at[cvs].set(jnp.arange(config.n_context_venues))

is_context = jnp.zeros(n, dtype=jnp.bool_).at[cvs].set(True)

priorities = jnp.where(is_context, priorities, jnp.arange(n) + n)

perm = jnp.argsort(priorities)

inv_perm = jnp.argsort(perm)

def get_permuted_weights():

J = jnp.zeros((n, n)).at[triu_idx].set(state.weights)

J = J + J.T

J_p = J[perm][:, perm]

return J_p[triu_idx]

b_p = state.biases[perm]

w_p = lax.cond(jnp.all(perm == jnp.arange(n)), lambda: state.weights, get_permuted_weights)

# 2. Build model

model = IsingEBM(infra['nodes'], infra['edges'], b_p, w_p, jnp.array(config.beta))

updated_prog = IsingSamplingProgram(

model,

infra['prog'].gibbs_spec.superblocks,

infra['prog'].gibbs_spec.clamped_blocks

)

clamped_state = [(cos > 0).astype(jnp.bool_)]

k_init, k_sample, k_tie = random.split(key, 3)

init = hinton_init(k_init, model, updated_prog.gibbs_spec.free_blocks, ())

samples = sample_states(k_sample, updated_prog, infra['sched'], init, clamped_state, infra['full_block'])[0]

# 3. Decode results

spins = (2 * samples.astype(jnp.float32) - 1).reshape(samples.shape[0], -1)[:, inv_perm]

margs = jnp.mean(spins, axis=0)

probs = (margs + 1) / 2

routing_mask = jnp.zeros(n).at[cvs].set(-1e9)

# k_tie already assigned via split above

return select_among_max(k_tie, probs, routing_mask), probs

def thrml_sample_joint(state, key, infra, config):

"""Perform UNCLAMPED sampling for unbiased weight updates."""

model = IsingEBM(infra['nodes'], infra['edges'], state.biases, state.weights, jnp.array(config.beta))

updated_prog = IsingSamplingProgram(

model,

infra['joint_prog'].gibbs_spec.superblocks,

infra['joint_prog'].gibbs_spec.clamped_blocks

)

k1, k2 = random.split(key)

init = hinton_init(k1, model, updated_prog.gibbs_spec.free_blocks, ())

samples = sample_states(k2, updated_prog, infra['sched'], init, [], infra['full_block'])[0]

spins = (2 * samples.astype(jnp.float32) - 1).reshape(samples.shape[0], -1)

node_moms = jnp.mean(spins, axis=0)

edge_moms = ((spins.T @ spins) / config.n_samples)[jnp.triu_indices(state.biases.shape[0], 1)]

return node_moms, edge_momsdef run_one_seed(seed, config, data, infra):

n = config.n_venues; act_steps = data.shape[0]

def step(carry, step_idx):

rng, s_ceg, s_cts, s_thrml = carry

step_data = data[step_idx]

out_rewards = step_data[:n]

out_states = step_data[n:]

rng, k_c, k_a, k_u = random.split(rng, 4)

is_fixed = (config.context_mode == "fixed")

# Fetch multiple context venues

cvs = lax.cond(

is_fixed,

lambda: jnp.arange(config.n_context_venues),

lambda: jax.random.permutation(k_c, jnp.arange(n))[:config.n_context_venues]

)

cos = out_states[cvs]

cidx = get_context_index(cvs, cos, n, config.n_context_venues)

routing_mask = jnp.zeros(n).at[cvs].set(-1e9)

oracle_best = jnp.argmax(out_rewards + routing_mask); oracle_rew = out_rewards[oracle_best]

k_ceg, k_cts, k_thrml = random.split(k_a, 3)

act_ceg = ceg_select(s_ceg, k_ceg, cidx, routing_mask)

act_cts = cts_select(s_cts, k_cts, cidx, routing_mask)

a_thrml, _ = thrml_select_conditional(s_thrml, k_thrml, cvs, cos, infra, config)

model_node_moms, model_edge_moms = thrml_sample_joint(s_thrml, k_u, infra, config)

regret = oracle_rew - jnp.array([out_rewards[act_ceg], out_rewards[act_cts], out_rewards[a_thrml]])

next_ceg = ceg_update(s_ceg, cidx, act_ceg, out_rewards[act_ceg], config.discount_factor)

next_cts = cts_update(s_cts, cidx, act_cts, out_rewards[act_cts], config.discount_factor)

obs_mask = jnp.zeros(n).at[cvs].set(1.0).at[a_thrml].set(1.0)

next_thrml = thrml_update(s_thrml, out_states * obs_mask, obs_mask, model_node_moms, model_edge_moms,

config.discount_factor, config.beta, config.learning_rate,

config.propagation_damping, config.damp_coupling)

return (rng, next_ceg, next_cts, next_thrml), regret

initial_carry = (seed, ceg_init(config), cts_init(config), thrml_init(n, config.window_size))

final_carry, results = jax.lax.scan(step, initial_carry, jnp.arange(act_steps))

return {

"Contextual ε-Greedy": jnp.cumsum(results[:, 0]),

"Contextual Thompson Sampling": jnp.cumsum(results[:, 1]),

"THRML": jnp.cumsum(results[:, 2]),

"thrml_biases": final_carry[3].biases,

"thrml_weights": final_carry[3].weights

}def execute_experiment():

print(f"[START] Fetching Historical Data...")

print(f" Time window: {HIST_START_MS} to {HIST_END_MS}")

# Fetch historical trades from each exchange

dfs = {ex: sync_trades_hist(ex, HIST_START_MS, HIST_END_MS) for ex in EXCHANGES}

# Process the historical data

raw_data, raw_prices = process_market_data(dfs, HIST_START_MS, HIST_END_MS)

if raw_data.size == 0:

print("[ERROR] No data retrieved. Check your timestamps and try again.")

return

data = jnp.array(raw_data)

print(f"[DATA] Dataset Final Size: {data.shape[0]} bucketted seconds.")

config = ExperimentConfig(n_steps=data.shape[0], n_venues=len(EXCHANGES)); infra = build_thrml_infra(config.n_venues, config)

seeds = random.split(random.key(42), config.n_seeds)

labels = ["Contextual ε-Greedy", "Contextual Thompson Sampling", "THRML"]; summary = {}

# BATCHING SETTINGS TO PREVENT CUDA OOM

BATCH_SIZE = 50

jax.clear_caches()

n_total_seeds = config.n_seeds

for mode_name in ["fixed", "random"]:

conf = config._replace(context_mode=mode_name)

print(f"[RUN] Running {mode_name.upper()} Context (Batched execution to prevent OOM)... ")

# Initialize storage for batched results

all_res_list = []

# Compile runner inside jit for a single batch to keep graph smaller

runner = jit(vmap(lambda s: run_one_seed(s, conf, data, infra)))

start_time = time.time()

for i in range(0, n_total_seeds, BATCH_SIZE):

batch_seeds = seeds[i : i + BATCH_SIZE]

print(f" - Processing seeds {i} to {i + len(batch_seeds)}...", end="")

batch_start = time.time()

res = runner(batch_seeds)

# Ensure computation for this batch is done and clear from GPU staging

res = jax.tree_util.tree_map(lambda x: x.block_until_ready(), res)

all_res_list.append(res)

print(f" [{time.time()-batch_start:.1f}s]")

# Combine results across batches

batch_res = {}

for lbl in labels:

batch_res[lbl] = jnp.concatenate([r[lbl] for r in all_res_list], axis=0)

batch_res["thrml_biases"] = jnp.concatenate([r["thrml_biases"] for r in all_res_list], axis=0)

batch_res["thrml_weights"] = jnp.concatenate([r["thrml_weights"] for r in all_res_list], axis=0)

print(f" [DONE] Total Context mode completed in {time.time()-start_time:.1f}s")

summary[mode_name] = jnp.array([jnp.mean(batch_res[lbl][:, -1]) for lbl in labels])

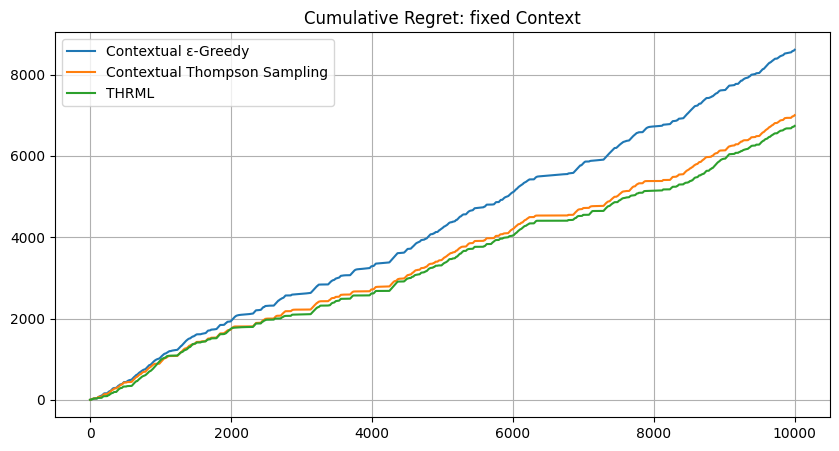

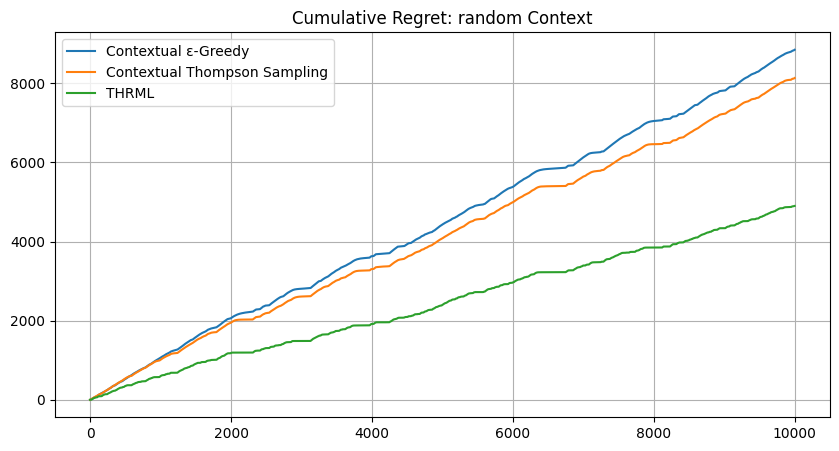

plt.figure(figsize=(10, 5))

for i, lbl in enumerate(labels):

plt.plot(jnp.mean(batch_res[lbl], axis=0), label=lbl)

plt.title(f"Cumulative Regret: {mode_name} Context"); plt.legend(); plt.grid(True);import os

os.makedirs('images', exist_ok=True)

plt.savefig(f'images/real_data_{mode_name}_regret.png'); plt.show()

if mode_name == "random":

global_final_biases = jnp.mean(batch_res["thrml_biases"], axis=0)

global_final_weights = jnp.mean(batch_res["thrml_weights"], axis=0)

print("" + "="*45)

print(f"{ 'MODE':<10} | { 'Contextual ε-Greedy':<10} | {'Contextual Thompson Sampling':<10} | {'THRML':<10}")

for m, v in summary.items():

print(f"{m:<10} | {float(v[0]):<10.2f} | {float(v[1]):<10.2f} | {float(v[2]):<10.2f}")

print("=" * 45)

return data, global_final_biases, global_final_weights, infra, config, raw_prices# Run the experiment

data, final_biases, final_weights, infra, config, prices = execute_experiment()[START] Fetching Historical Data...

Time window: 1773837750372 to 1773847750372

+ binanceus : Fetched 609 trades (3 API calls).

+ coinbaseexchange: Fetched 2479 trades (4 API calls).

+ kraken : Fetched 1592 trades (2 API calls).

+ bitfinex : Fetched 3160 trades (4 API calls).

+ bitstamp : Fetched 120 trades (1 API calls).

[DATA] Processing 10000 time buckets (1773837750372 to 1773847750372)

[COVERAGE] binanceus : 9875.9s of 10000s ( 98.8%)

[COVERAGE] coinbaseexchange: 9938.1s of 10000s ( 99.4%)

[COVERAGE] kraken : 9993.6s of 10000s ( 99.9%)

[COVERAGE] bitfinex : 9988.7s of 10000s ( 99.9%)

[COVERAGE] bitstamp : 9579.0s of 10000s ( 95.8%)

binanceus: 609 trades mapped to buckets (causal fill from bucket 12)

coinbaseexchange: 2479 trades mapped to buckets (causal fill from bucket 11)

kraken: 1592 trades mapped to buckets (causal fill from bucket 5)

bitfinex: 3160 trades mapped to buckets (causal fill from bucket 2)

bitstamp: 120 trades mapped to buckets (causal fill from bucket 47)

[DATA] Dropping 2 leading buckets with no observed venue prices.

[DATA] Dataset Final Size: 9998 bucketted seconds.

[RUN] Running FIXED Context (Batched execution to prevent OOM)...

- Processing seeds 0 to 50... [225.2s]

- Processing seeds 50 to 100... [202.3s]

- Processing seeds 100 to 150... [202.2s]

- Processing seeds 150 to 200... [202.3s]

[DONE] Total Context mode completed in 832.2s

[RUN] Running RANDOM Context (Batched execution to prevent OOM)...

- Processing seeds 0 to 50... [222.6s]

- Processing seeds 50 to 100... [200.7s]

- Processing seeds 100 to 150... [200.7s]

- Processing seeds 150 to 200... [200.6s]

[DONE] Total Context mode completed in 824.7s

=============================================

MODE | Contextual ε-Greedy | Contextual Thompson Sampling | THRML

fixed | 8610.59 | 7002.17 | 6738.68

random | 8848.45 | 8134.47 | 4901.35

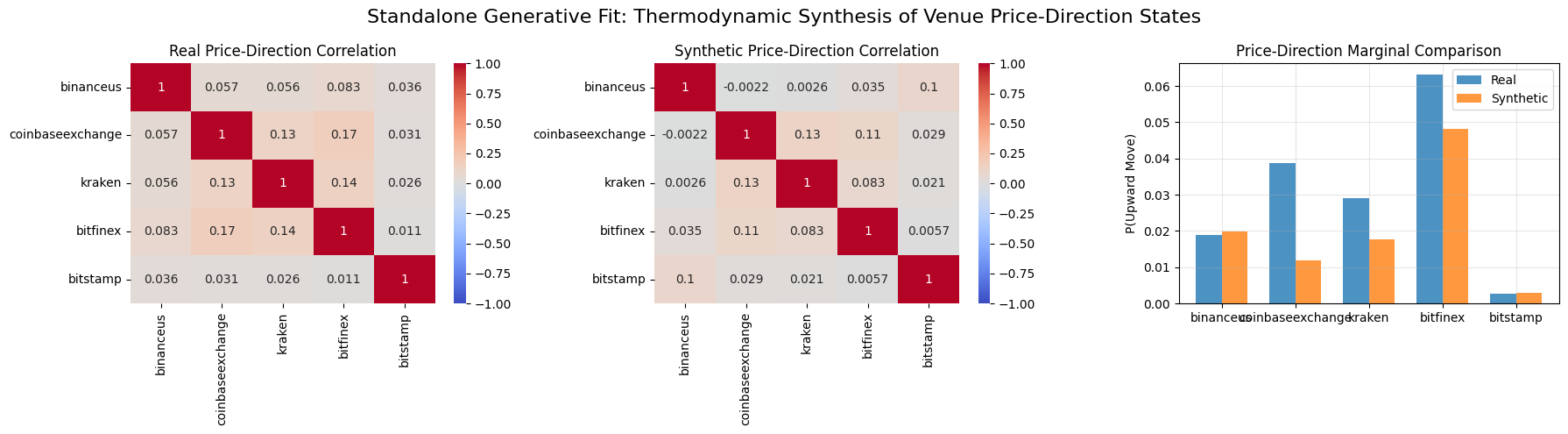

=============================================This section is a separate standalone generative experiment, not a validation of the routing agent’s learned state.

Starting from the raw exchange price series fetched above, we derive a binary price-direction state for each venue at each timestep (\(+1\) if the next price move is upward, \(-1\) otherwise). We then train a fresh Ising EBM on these fully observed price-direction states using unclamped model sampling for the negative phase.

This target distribution is different from the routing experiment above. The routing benchmark learns from competitive winner labels (exactly one venue receives \(+1\) per timestep under the sell-side routing objective), whereas this generative side experiment models market direction co-movements across venues. The goal here is therefore to assess whether THRML can fit and sample from the correlation structure of price-direction states, rather than to claim that the routing agent itself becomes a generative model.

import seaborn as sns

def generate_synthetic_data(biases, weights, n_samples, infra, config):

print(f"Generating {n_samples} synthetic price-direction states using unclamped Gibbs sampling...")

model = IsingEBM(infra['nodes'], infra['edges'], biases, weights, jnp.array(config.beta))

# Recreate program based on static unclamped joint program blocks

prog = IsingSamplingProgram(

model,

infra['joint_prog'].gibbs_spec.superblocks,

clamped_blocks=[]

)

# Use trained steps_per_sample to ensure adequate mixing and decorrelation

sched = SamplingSchedule(n_warmup=100, n_samples=n_samples, steps_per_sample=config.steps_per_sample)

k1, k2 = random.split(random.key(42))

init = hinton_init(k1, model, prog.gibbs_spec.free_blocks, ())

samples = sample_states(k2, prog, sched, init, [], infra['full_block'])[0]

spins = 2 * samples.astype(jnp.float32) - 1

return spins.reshape(n_samples, -1)

# 1. Build a standalone generative dataset from venue price directions

# Trim the leading sentinel-only prefix so the generative model trains on fully observed causal prices.

valid_rows = np.all(prices > 0, axis=1)

if not np.any(valid_rows):

raise ValueError("No fully observed price rows are available for the standalone generative experiment.")

first_fully_observed_row = int(np.argmax(valid_rows))

trimmed_prices = prices[first_fully_observed_row:]

print(

f"Using price rows {first_fully_observed_row}..{prices.shape[0] - 1} "

f"for the standalone generative experiment ({trimmed_prices.shape[0]} fully observed buckets)."

)

price_diffs = np.diff(trimmed_prices, axis=0)

gen_states = jnp.array(np.where(price_diffs > 0, 1.0, -1.0))

# 2. Standalone unsupervised training loop over fully observed price-direction states

def train_generative_model(config, infra, states):

def step(carry, state_obs):

rng, s_thrml = carry

rng, k_u = random.split(rng)

# Unclamped sampling to get model moments

model_node_moms, model_edge_moms = thrml_sample_joint(s_thrml, k_u, infra, config)

# Fully observed update on price-direction states with stationary discounting

obs_mask = jnp.ones(config.n_venues)

next_thrml = thrml_update(

s_thrml, state_obs, obs_mask, model_node_moms, model_edge_moms,

1.0, config.beta, config.learning_rate,

config.propagation_damping, config.damp_coupling

)

return (rng, next_thrml), None

init_state = thrml_init(config.n_venues, config.window_size)

(final_rng, trained_gen_model), _ = jax.lax.scan(step, (random.key(99), init_state), states)

return trained_gen_model

print("Training standalone generative EBM on price-direction correlations...")

gen_model = train_generative_model(config, infra, gen_states)

# 3. Generate synthetic price-direction states using the dedicated generative model

synthetic_data = generate_synthetic_data(gen_model.biases, gen_model.weights, 5000, infra, config)Using price rows 45..9997 for the standalone generative experiment (9953 fully observed buckets).

Training standalone generative EBM on price-direction correlations...

Generating 5000 synthetic price-direction states using unclamped Gibbs sampling...# Extract the price-direction state observations for comparison

real_states = gen_states

# 1. Marginal Probabilities (P(Upward Move))

real_marginals = (np.mean(real_states, axis=0) + 1) / 2

synthetic_marginals = (np.mean(synthetic_data, axis=0) + 1) / 2

marg_mae = np.mean(np.abs(real_marginals - synthetic_marginals))

marg_mse = np.mean((real_marginals - synthetic_marginals)**2)

# 2. Pairwise Correlations

real_cov = np.corrcoef(real_states, rowvar=False)

synthetic_cov = np.corrcoef(synthetic_data, rowvar=False)

corr_mae = np.mean(np.abs(real_cov - synthetic_cov))

corr_mse = np.mean((real_cov - synthetic_cov)**2)

# 3. Visualization

fig, axes = plt.subplots(1, 3, figsize=(18, 5))

# Heatmap Real

sns.heatmap(real_cov, annot=True, cmap="coolwarm", center=0, ax=axes[0],

xticklabels=EXCHANGES, yticklabels=EXCHANGES, vmin=-1.0, vmax=1.0)

axes[0].set_title("Real Price-Direction Correlation")

# Heatmap Synthetic

sns.heatmap(synthetic_cov, annot=True, cmap="coolwarm", center=0, ax=axes[1],

xticklabels=EXCHANGES, yticklabels=EXCHANGES, vmin=-1.0, vmax=1.0)

axes[1].set_title("Synthetic Price-Direction Correlation")

# Marginal Bar Plot

x = np.arange(len(EXCHANGES))

width = 0.35

axes[2].bar(x - width/2, real_marginals, width, label='Real', color='#1f77b4', alpha=0.8)

axes[2].bar(x + width/2, synthetic_marginals, width, label='Synthetic', color='#ff7f0e', alpha=0.8)

axes[2].set_xticks(x)

axes[2].set_xticklabels(EXCHANGES)

axes[2].set_ylabel('P(Upward Move)')

axes[2].set_title('Price-Direction Marginal Comparison')

axes[2].legend()

axes[2].grid(True, alpha=0.3)

plt.suptitle("Standalone Generative Fit: Thermodynamic Synthesis of Venue Price-Direction States", fontsize=16)

plt.tight_layout()

import os

os.makedirs('images', exist_ok=True)

plt.savefig('images/generative_ai_heatmap.png')

plt.show()

print("=" * 65)

print("STANDALONE GENERATIVE VALIDATION ON PRICE-DIRECTION STATES")

print("=" * 65)

print(f"Marginal Probabilities MAE: {marg_mae:.4f}")

print(f"Marginal Probabilities MSE: {marg_mse:.4f}")

print("-" * 65)

print(f"Correlation Matrix MAE: {corr_mae:.4f}")

print(f"Correlation Matrix MSE: {corr_mse:.4f}")

print("=" * 65)

print("This section evaluates a fresh generative model trained on price-direction states, not the routing agent.")

=================================================================

STANDALONE GENERATIVE VALIDATION ON PRICE-DIRECTION STATES

=================================================================

Marginal Probabilities MAE: 0.0108

Marginal Probabilities MSE: 0.0002

-----------------------------------------------------------------

Correlation Matrix MAE: 0.0283

Correlation Matrix MSE: 0.0016

=================================================================

This section evaluates a fresh generative model trained on price-direction states, not the routing agent.